Most partners think their matter budgets are fine until they try to reconcile them at year-end. That's when you find the associate who billed 47 hours to "research" on a straightforward contract review. Or the paralegal time that somehow got coded to three different cost centers. Or the partner who approved a $28,000 expert witness fee that was never in the original budget.

The real problem isn't that lawyers are bad at budgeting. Most firms are running modern practices with frameworks built for 1995. Partners on personal Excel templates, associates guessing at time allocations, nobody tracking whether fixed costs on Matter A are eating into the margins on Matter B.

The firms that actually make money consistently aren't the ones with sophisticated financial models. They're the ones with dead-simple cost taxonomies that everyone actually uses.

Why traditional matter budgets fail at the worst possible moment

A mid-sized firm lands a complex litigation matter. The partner creates a budget in Excel, breaks it down by phase—discovery, motion practice, trial prep—and everyone nods along. Six months later, the client gets a bill that's 40% over budget, the partner has no idea where the overage came from, and the associate who did most of the work has already moved to another firm.

The breakdown almost always starts with cost categorization. Most firms lump everything into broad buckets like "attorney time" or "expenses." But when you're trying to figure out why realization on litigation dropped from 87% to 71% last quarter, those categories tell you nothing.

A firm in Dallas discovered they were losing around $1,800 per matter on poorly allocated research database costs. They were treating Westlaw access as fixed overhead and spreading it evenly across all matters. Meanwhile, their corporate team barely touched it while litigation was running massive searches daily. Once they moved to usage-based allocation, the true cost structure became obvious—and so did which matters were actually profitable.

The taxonomy problem gets worse when you factor in shared resources. IT support, office manager, marketing coordinator—these aren't direct matter costs, but they're not pure overhead either. The IP boutique that treats them as overhead ends up subsidizing high-maintenance clients with profits from efficient ones. The employment firm that tries to allocate them precisely spends more on tracking than they save on accuracy. Neither approach works.

Building a cost-driver taxonomy that actually works

Start with your cost drivers, not your costs. Most firms do this backwards—they list all their expenses and then try to figure out allocation. Instead, identify what actually drives costs in your practice:

Never miss a critical deadline again.

Casioly helps legal teams manage cases efficiently and stay on top of critical tasks.

- Centralized case tracking

- Automated deadline reminders

- Secure client communication

No credit card required

Direct Matter Drivers

-

Timekeeper hours (by level)

-

Document volume (for discovery-heavy matters)

-

Court appearances (including travel)

-

Expert witnesses and consultants

-

Filing fees and court costs

Complexity Multipliers

-

Number of parties involved

-

Jurisdictional requirements

-

Regulatory oversight level

-

Client communication frequency

-

Document production requirements

Operational Overhead Drivers

-

Technology usage (per matter, not per month)

-

Administrative support hours

-

Supervision and review time

-

Knowledge management contributions

Notice what's not on this list? Generic categories like "overhead" or "miscellaneous expenses." Every cost needs a driver, and every driver needs an owner.

A boutique litigation firm using this taxonomy can predict matter profitability within roughly 8% accuracy after the initial client meeting—not because they're financial wizards, but because they've identified their actual cost drivers instead of relying on generic accounting categories.

Stage-based budget templates that prevent scope creep

The worst budget overruns happen at transitions between matter stages. Discovery bleeds into motion practice. Document review extends into trial prep. Before you know it, you're explaining to a client why their "simple contract dispute" consumed 340 billable hours.

A stage-based template structure that actually prevents this:

| Matter Stage | Fixed Costs | Variable Costs | Trigger for Next Stage |

|---|---|---|---|

| Initial Assessment | $2,500–3,500 (partner review, conflict check, intake) | $0 | Engagement letter signed |

| Pre-filing Investigation | $5,000 (flat) | $150–250/hr for additional research | Complaint drafted |

| Discovery Phase | $8,000 (base discovery package) | $2,000 per 10GB documents reviewed | Discovery close date |

| Motion Practice | $12,000 per dispositive motion | $3,000 per discovery motion | Trial date set |

| Trial Preparation | $25,000 (base prep) | $5,000/day of trial | Verdict/settlement |

The key isn't the specific numbers—yours will be different. It's the structure. Fixed costs for predictable work, variable costs for scope-dependent work, and clear triggers that define when you've moved to the next stage.

This connects directly to matter lifecycle management, which determines when stages actually transition and what data you need at each point. Without clear stage definitions, budgets become moving targets.

One employment law firm started using stage-based budgets and saw their realization rate jump from around 79% to 91% in eight months. Not because they got better at the law—because they stopped letting matters drift between stages without anyone noticing.

Fixed vs. variable vs. shared cost allocation

Most firms treat cost allocation like an accounting exercise. It's not. It's an operational decision that affects matter acceptance, associate utilization, and partner compensation.

Fixed costs are the easiest to handle wrong. Office lease, malpractice insurance, practice management software—these feel fixed because you pay them monthly. But allocating them evenly across matters means your two-week research project is subsidizing your two-year litigation.

What actually works: allocate fixed costs based on predicted resource consumption, not time. A complex merger uses more firm resources than a simple will, even if the will takes more calendar days.

Variable costs should be variable in allocation too. That sounds obvious, but watch what happens when firms try to standardize. They create rules like "all matters get charged 2% for technology costs" when e-discovery might be 15% of costs for litigation and 0% for estate planning.

Shared costs are where firms really struggle. A paralegal who supports three partners is the classic example. Most firms either divide their time equally (wrong—one partner might generate 70% of the work), track every six-minute increment (wrong—the overhead exceeds the benefit), or treat them as pure overhead (wrong—you lose visibility into matter profitability).

Usage-based allocation with reasonable approximations solves this. Track at the week level, not the minute level. Review quarterly, not daily.

Track at the week level, not the minute level.

A firm in Phoenix found their highest-margin partner was actually their lowest when shared costs were properly allocated. He was consuming roughly 60% of paralegal time while generating 35% of revenue. Once they could see it, they could fix it.

Partner accountability without destroying firm culture

Partner accountability around budgets is mostly theater in small and mid-sized firms. Everyone knows who the chronic overrunners are, but nobody wants to say it out loud. So firms build elaborate tracking systems nobody uses and reports nobody reads.

Real accountability comes from visibility, not punishment. Make the data impossible to ignore without making it feel like surveillance.

Matter Budget Status Check

-

Current hours vs. budgeted hours (by stage)

-

External costs incurred vs. approved

-

Upcoming costs requiring approval

-

Client communication needed (Y/N)

No complex variance analysis. No detailed explanations. Just four data points that tell you whether a matter is on track.

The enforcement mechanism isn't punitive—it's procedural. Matters over 15% of budget automatically flag for client communication. Matters over 25% require partner review before additional work continues. Matters over 40% trigger a formal budget revision with client approval.

One firm started showing each partner's budget accuracy rate at monthly meetings—not to shame anyone, just a simple percentage: "Jim hit 87% last month, Sarah hit 94%." Within three months, every partner was hitting 85% or better. Lawyers are naturally competitive. Nobody wants to be the outlier.

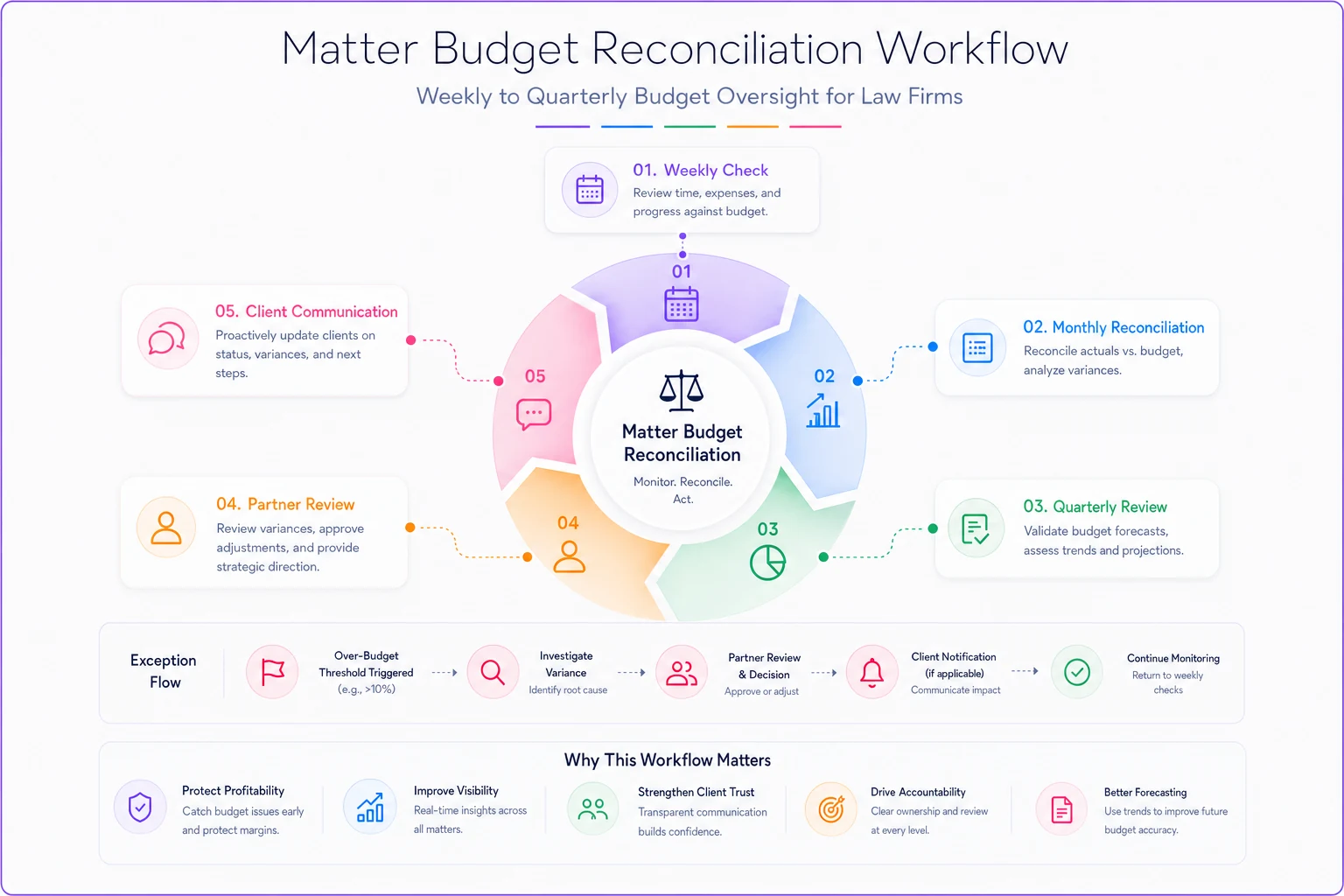

The reconciliation checklist that catches problems before clients do

Most budget reconciliations happen too late—after the bill goes out, after the client complains, after the write-off. Firms that maintain high realization rates reconcile continuously, but they do it smart, not obsessively.

Weekly (5 minutes per matter):

-

Hours entered vs. hours worked (catch missing time)

-

Cost codes used (catch miscategorization)

-

Upcoming deliverables vs. remaining budget

Monthly (15 minutes per matter):

-

Budget consumption rate vs. matter completion rate

-

Shared cost allocations vs. actual usage

-

Client communication log vs. budget status

Quarterly (30 minutes per matter):

-

Full budget-to-actual reconciliation

-

Profitability analysis including all costs

-

Adjustments for next quarter

The key is making reconciliation part of operations, not a separate accounting exercise. Linking it to your operational dashboards means partners see budget status alongside other matter metrics—not buried in a separate system they open twice a year.

A simple workflow like this keeps reconciliation routine and visible without being burdensome.

A real scenario: How one firm fixed their broken budget process

A 12-attorney insurance defense firm was losing money on what should have been profitable matters. Billing around $3.2 million annually, realization rate at 71% and still falling.

The problem wasn't one thing—it was everything. Partners used different budget templates. Associates didn't know what category to bill research time. Shared costs were allocated based on a formula from 2015. Nobody reconciled anything until a matter closed.

They made three changes.

First, they standardized on a single cost taxonomy with 12 categories total. Not perfect, but usable. Everyone knew where everything went.

Second, they built stage-based budget templates for their four main practice areas, with fixed and variable costs and clear triggers for stage transitions.

Third, they required weekly five-minute reconciliations. Not detailed reviews—quick checks to catch obvious problems before they became expensive ones.

Month one, they found around $47,000 in miscategorized time. Month two, they caught three matters trending toward 50% overruns while there was still time to act. Month six, realization hit 86%.

The real win was operational, though. Partners stopped avoiding budget conversations. Associates stopped guessing at time entries. Clients stopped being surprised by invoices.

The software piece nobody talks about

Most firms try to solve budgeting problems with more sophisticated software. They buy elaborate practice management systems with complex budgeting modules, then wonder why adoption is poor and the problems persist.

The issue isn't the software—it's the workflow. If your budgeting process requires seventeen screens and perfect data entry, it will fail regardless of the technology behind it.

What actually works is AI-powered operational software that handles categorization and allocation automatically—not replacing human judgment, but eliminating the manual work that makes people skip the process entirely.

Modern platforms can read time entries and assign them to the correct cost categories, track document volumes and allocate e-discovery costs accordingly, and monitor matter stages to flag when budgets need updating. The automation doesn't replace the framework—it enforces it. When every time entry gets properly categorized and every reconciliation happens without someone having to manually trigger it, the framework actually holds up in practice instead of quietly falling apart after month two.

A matter budgeting framework isn't about perfection. It's about visibility and consistency—knowing where money is going, whether matters are profitable, and when to have difficult conversations with clients before those conversations become arguments about write-offs.

Start small. Pick five active matters and apply the framework for one month. Use the cost-driver taxonomy. Create simple stage-based budgets. Run weekly reconciliations. See what breaks.

The firms that get this right aren't the ones with the most complex systems. They're the ones where everyone uses the same simple system, consistently—where partners can't hide behind bad data, where associates understand how their time affects profitability, where clients trust the bills because the budgets actually mean something.

Your matter budgeting framework is really just an operational agreement about how you track and allocate costs. Make it simple enough that everyone actually uses it, detailed enough that it provides real insight, and automated enough that it doesn't become another task that quietly gets skipped when things get busy. The alternative is what most firms have right now: sophisticated budgets nobody follows, allocation rules nobody understands, and recurring surprise when profitable matters lose money. That's not a budgeting problem—it's an operational one, and it's fixable.

Ready to elevate your legal practice management?

Join 500+ law firms using Casioly to optimize case workflows, reduce administrative burden, and improve client satisfaction.